- Sign in

-

Don't have an account? Join QuantConnect Today

- Sign up for Free

SIGN IN

Welcome to

Algorithm Lab

We are dedicated to providing investors with a cutting-edge platform for rapidly creating quant investment strategies. Founded in 2012, we've empowered more than 500,000 quants and engineers to create and trade their ideas.

Automated and Supercharged Research

Agentic AI Assistants

We've deployed the cutting edge of AI technology at your fingertips. Harness teams of AI quant researchers and coders to automate your research process, backtesting, and trading.

Your Quantitative Foundation

Learning Center

Quickly and easily started with our API to build your strategy. The learning center lessons are interactive, step-by-step guides to make you productive as fast as possible.

Explore Free and Paid Datasets

Vast Datasets

Focus your efforts on driving alpha, not parsing CSV files. Our cloud offers hundreds of terabytes of traditional and alternative data preformatted, cleaned, and instantly accessible by our API.

Collaborate with Your Team

Organizations

Coordinate teamwork, control access permissions, and your shared cloud resources. Grow your trading organization safely and efficiently on top of our cloud architecture.

Jumpstart Your Algorithm Development

Strategy Explorer

A selection of streaming live-trading strategies written by QuantConnect, and top highlights from the community available to follow and clone. Peer into detailed real-time positions to gain insight for your own trading.

Loading Algorithm Lab v3.0...

Begin Your QuantConnect Journey

Algorithm Lab is your playground for developing and refining trading algorithms with QuantConnect. Utilize advanced tools, historical data, and robust backtesting to enhance your trading strategies. Transform your ideas into actionable insights and optimize your trading approach with ease.

Sign Up for FreeAlready have an account Log In.

Quant Developer

Trial Only - Limited Time Special

Upgrade to an annual plan before your trial expires , to get an additional month free, saving a total of compared to our monthly plans.

! Let’s Get Started.

Choose a method below to begin building your prompt.

Dictate your strategy to Mia to implement.

Step-by-step guided prompt creation.

Generate a prompt from a random idea.

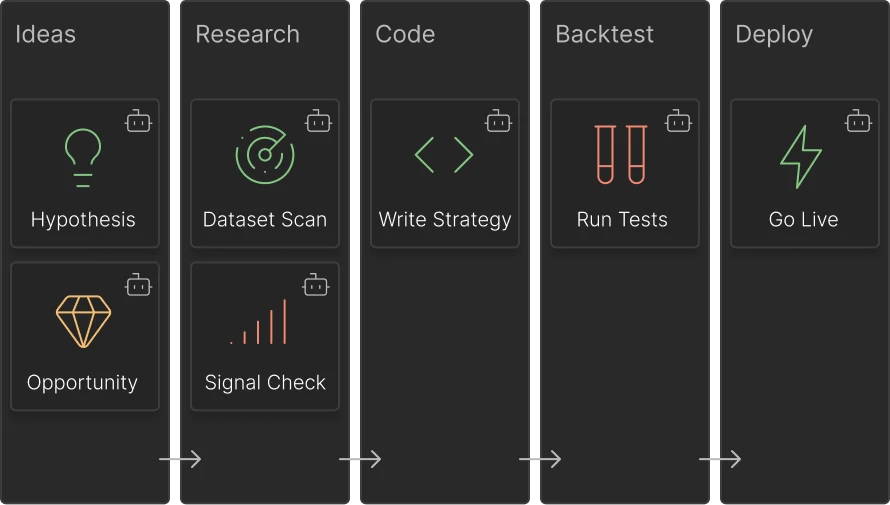

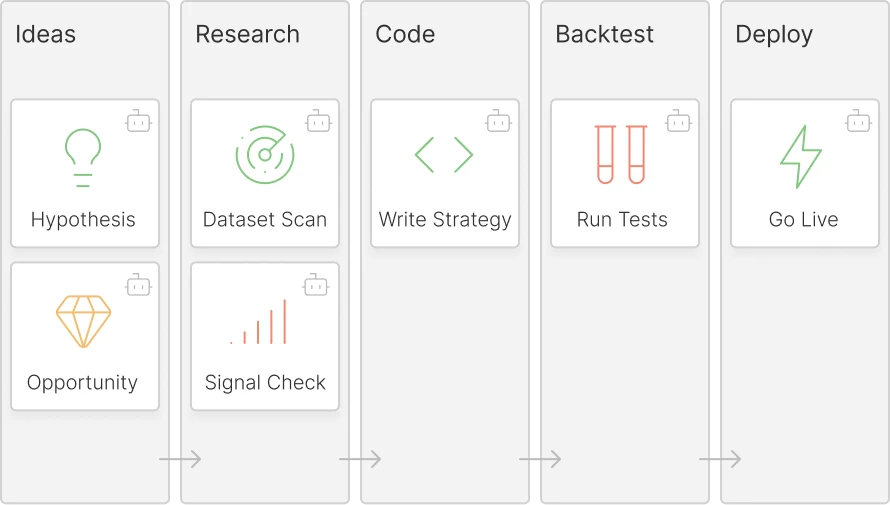

Research Pipeline

Input Required

Error

Running

Completed

Start

NEW ALGORITHM

-

Build With AI

Build your algorithm using the research pipeline.

-

Code From Template

Code your own strategy or start from our templates.

Code Environments

Pinned Projects

You haven't created any projects yet.

Create Your First ProjectLoading recent projects...

You haven't created any projects yet.

Click here to Create Your First ProjectMy Projects

Home >

Project Name

Collaborators

Modified

Pinned Projects

- Page of

Cancellation Scheduled. You have access to QuantConnect until .

Organization Notes

Get Started with Algorithm Lab

New Research

Sizing Market Exposure With Aggregate Sales Growth

Use aggregate sales growth to time SPY/BIL market exposure...

ReadWhat brings you here today?

You can harness AI to research, backtest, and live trade almost any idea, or explore strategies created by the community. Advanced users can dive into the strategy code to customize it.

Research Assistant

The research assistant can pull on our data and infrastructure to test your investment ideas to confirm the statistical foundation.

Backtest Assistant

Quickly implement the code for your ideas for a realistic, point-in-time backtest powered by QuantConnect's data and infrastructure.

Live Risk Monitoring

The live assistant will monitor your portfolio, track risks from breaking news and market shocks, and send you regular alerts about your exposure.

I have an idea I want to test

Research, backtest, and paper-trade your ideas on our powerful cloud quant platform.

Perform Preliminary Research on Idea

Explore the statistical strength of an idea by describing your idea to our AI Quant Researcher.

Create Backtest from an Idea

Describe your idea and our AI systems will implement it using the QuantConnect API.

Implement Idea Manually with Python or C#

For full control and oversight implement your ideas against the QuantConnect API.

I'm looking for new ideas to trade

Browse community algorithms for inspiration, or read ideas based on the latest research.

Strategy Builder

Explore what is possible with a guided, no-code, strategy builder.

Explore Strategy Library

Browser through strategies created by the community including latest out of sample performance.

Welcome Video

A quick note from the founder to welcome you to QuantConnect.

Product Tour Video

Take a tour of the highlights to see what’s possible with QuantConnect.

Templates

No templates match the current filter.

No Coding Session Available

Retry

No Coding Session Available

Retry

| NAME | ORGANIZATION | |

|---|---|---|

Upgrade Coding Environment

Your account is currently paused

To continue using the platform, please resume billing.

Resume Billing

How would you rate your experience on QuantConnect?

⭑

⭑

⭑

⭑

⭑

Hover and click over the stars to rate us.

It looks like you are not fully satisfied with your experience on QuantConnect, please take a moment to let us know how we can improve our services for you:

We are glad you're enjoying QuantConnect!

If you have a minute to spare, please leave us a review on Trustpilot.

Stories like yours help others see the full potential of QuantConnect.

Please select one purchase option

Switch Organization

Create Organization

Create Organization

| Organization Name |

|---|

Update Billing Information

Update Billing Information

Upgrade to Team plan or higher to enable custom invoicing

Changes will be applied to future invoices.

Add members by sending them invitations to join your organization.

Copy Invite Link

Copy Invite Link

Add members by sending them invitations to join your organization.

Only organization administrators can invite new team members or generate invite links. To add a new member, ask your administrator to share an invite link.

Invitations Sent

Users will be able to join by following the link in the invitation email.

You’ve been invited by Jared Broad to join his G-Force Organization.

Would you like to accept the invitation?

Assign Seat

Rename Encryption Key

Delete Encryption Key

Caution: We will not be able to decrypt encrypted projects without the original key.

Caution: We will not be able to decrypt encrypted projects without the original key.

Add Encryption Key

Drag & Drop or

Keys are added to the local storage in your web browser and not uploaded to QuantConnect. To use an encrypted project on another computer you will need to bring a copy of the key.

Authorize

This project is encrypted using the key .

Authorize

This project will be encrypted using the key .

Add IP Address

Update IP Address

Delete IP Address

|

|

|

|||||||

|

||||||||

|

|

||||||||

|

|

||||||||