Option Strategies

Long Put Calendar Spread

Introduction

Put calendar spread, also known as put horizontal spread, is a combination of a longer-term (far-leg/front-month) put and a shorter-term (near-leg/back-month) put, where both puts have the same underlying stock and the same strike price. The long put calendar spread consists of buying a longer-term put and selling a shorter-term put. This strategy profits from a decrease in price movement. The strategy also profits from the time decay value because the theta $\theta$ (the Option price decay by 1 day closer to maturity) of the shorter-term put is larger than the longer-term put.

Implementation

Follow these steps to implement the long put calendar spread strategy:

- In the

Initializeinitializemethod, set the start date, end date, cash, and Option universe. - In the

OnDataon_datamethod, select the strike price and expiration dates of the contracts in the strategy legs. - In the

OnDataon_datamethod, call theOptionStrategies.PutCalendarSpreadmethod and then submit the order.

private Symbol _symbol;

public override void Initialize()

{

SetStartDate(2017, 2, 1);

SetEndDate(2017, 2, 19);

SetCash(500000);

UniverseSettings.Asynchronous = true;

var option = AddOption("GOOG", Resolution.Minute);

_symbol = option.Symbol;

option.SetFilter(universe => universe.IncludeWeeklys().Strikes(-1, 1).Expiration(0, 62));

} def initialize(self) -> None:

self.set_start_date(2017, 2, 1)

self.set_end_date(2017, 2, 19)

self.set_cash(500000)

self.universe_settings.asynchronous = True

option = self.add_option("GOOG", Resolution.MINUTE)

self._symbol = option.symbol

option.set_filter(lambda universe: universe.include_weeklys().strikes(-1, 1).expiration(0, 62))

public override void OnData(Slice slice)

{

if (Portfolio.Invested) return;

// Get the OptionChain

var chain = slice.OptionChains.get(_symbol, null);

if (chain == null || chain.Count() == 0) return;

// Get the ATM strike price

var atmStrike = chain.OrderBy(x => Math.Abs(x.Strike - chain.Underlying.Price)).First().Strike;

// Select the ATM put contracts

var puts = chain.Where(x => x.Strike == atmStrike && x.Right == OptionRight.Put);

if (puts.Count() == 0) return;

// Select the near and far expiration dates

var expiries = puts.Select(x => x.Expiry).OrderBy(x => x);

var nearExpiry = expiries.First();

var farExpiry = expiries.Last(); def on_data(self, slice: Slice) -> None:

if self.portfolio.invested: return

# Get the OptionChain

chain = slice.option_chains.get(self.symbol, None)

if not chain: return

# Get the ATM strike price

atm_strike = sorted(chain, key=lambda x: abs(x.strike - chain.underlying.price))[0].strike

# Select the ATM put contracts

puts = [i for i in chain if i.strike == atm_strike and i.right == OptionRight.PUT]

if len(puts) == 0: return

# Select the near and far expiration dates

expiries = sorted([x.expiry for x in puts], key = lambda x: x)

near_expiry = expiries[0]

far_expiry = expiries[-1]

var optionStrategy = OptionStrategies.PutCalendarSpread(_symbol, atmStrike, nearExpiry, farExpiry); Buy(optionStrategy, 1);

option_strategy = OptionStrategies.put_calendar_spread(self.symbol, atm_strike, near_expiry, far_expiry) self.buy(option_strategy, 1)

Option strategies synchronously execute by default. To asynchronously execute Option strategies, set the asynchronous argument to Falsefalse. You can also provide a tag and order properties to the

Buy method.

Buy(optionStrategy, quantity, asynchronous, tag, orderProperties);

self.Buy(option_strategy, quantity, asynchronous, tag, order_properties)

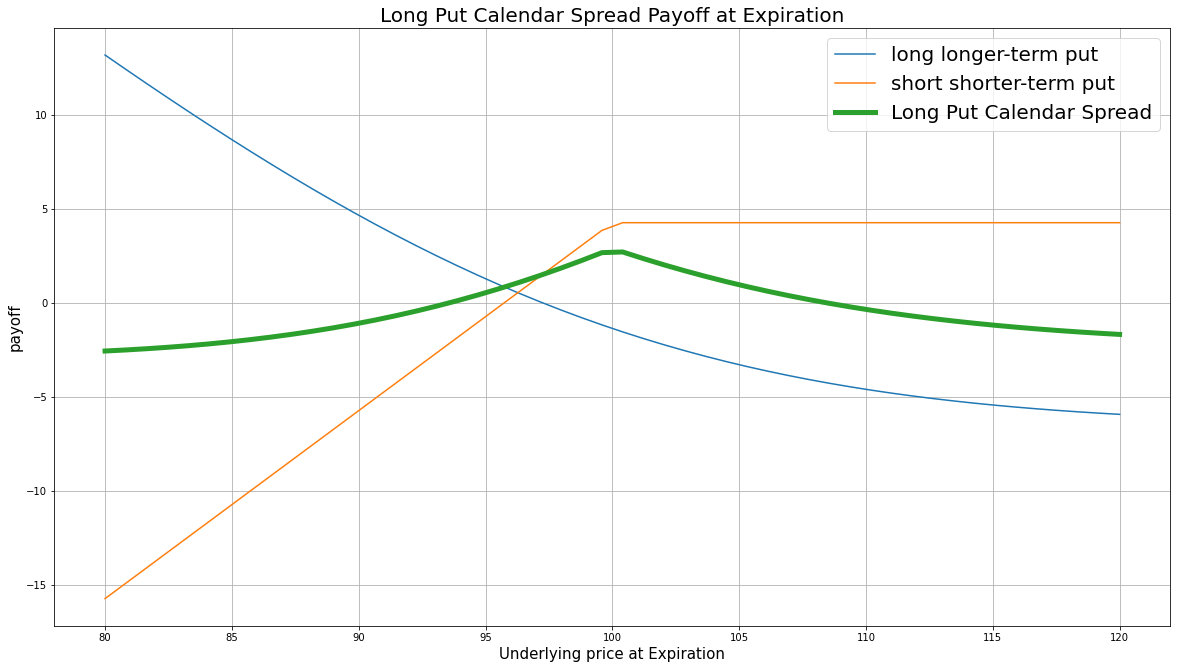

Strategy Payoff

The long put calendar spread is a limited-reward-limited-risk strategy. The payoff is taken at the shorter-term expiration. The payoff is

$$ \begin{array}{rcll} P^{\textrm{short-term}}_T & = & (K - S_T)^{+}\\ P_T & = & (P^{\textrm{long-term}}_T - P^{\textrm{short-term}}_T + P^{\textrm{short-term}}_0 - P^{\textrm{long-term}}_0)\times m - fee \end{array} $$ $$ \begin{array}{rcll} \textrm{where} & P^{\textrm{short-term}}_T & = & \textrm{Shorter term put value at time T}\\ & P^{\textrm{long-term}}_T & = & \textrm{Longer term put value at time T}\\ & S_T & = & \textrm{Underlying asset price at time T}\\ & K & = & \textrm{Strike price}\\ & P_T & = & \textrm{Payout total at time T}\\ & P^{\textrm{short-term}}_0 & = & \textrm{Shorter term put value at position opening (credit received)}\\ & P^{\textrm{long-term}}_0 & = & \textrm{Longer term put value at position opening (debit paid)}\\ & m & = & \textrm{Contract multiplier}\\ & T & = & \textrm{Time of shorter term put expiration} \end{array} $$The following chart shows the payoff at expiration:

The maximum profit is undetermined because it depends on the underlying volatility. It occurs when $S_T = S_0$ and the spread of the puts are at their maximum.

The maximum loss is the net debit paid, $P^{\textrm{short-term}}_0 - P^{\textrm{long-term}}_0$. It occurs when the underlying price moves very deep ITM or OTM so the values of both puts are close to zero.

If the Option is American Option, there is risk of early assignment on the sold contract. Naked long puts pose risk of losing all the debit paid if you don't close the position with short put together and the price drops below its strike.

Example

The following table shows the price details of the assets in the long put calendar spread algorithm:

| Asset | Price ($) | Strike ($) |

|---|---|---|

| Shorter-term put at position opening | 11.30 | 800.00 |

| Longer-term put at position opening | 19.30 | 800.00 |

| Longer-term put at shorter-term expiration | 3.50 | 800.00 |

| Underlying Equity at shorter-term expiration | 828.07 | - |

Therefore, the payoff is

$$ \begin{array}{rcll} P^{\textrm{short-term}}_T & = & (K - S_T)^{+}\\ & = & (800.00-828.07)^{+}\\ & = & 0\\ P_T & = & (P^{\textrm{long-term}}_T - P^{\textrm{short-term}}_T + P^{\textrm{short-term}}_0 - P^{\textrm{long-term}}_0)\times m - fee\\ & = & (3.50-0+11.30-19.30)\times100-1.00\times2\\ & = & -452\\ \end{array} $$So, the strategy losses $452.

The following algorithm implements a long put calendar spread Option strategy:

You can also see our Videos. You can also get in touch with us via Discord.

Did you find this page helpful?