Dear Community,

In a very hard decision, we've elected to cease support for the current version of Alpha Streams(v1.0) and focus our efforts on a new version that would implement a few core quant principles at its core (2.0).

The current submission and filtering process seeks strategies that perform well in all market regimes. This is a relatively unrealistic task and results in strong overfitting. A much more realistic approach is finding small factors which apply sometimes and swapping those factors in and out as regimes change with a global-macro/portfolio-level intelligence.

Additionally, providing too much information about the asset always led to selection bias. The new Alpha Streams universe will be a fixed portfolio of 5,000-6000 assets, anonymized, and scaled in value to 1.0 to help avoid this bias.

Keeping crowd-alpha accessible to investors is important to our mission, so we will build a way to bundle these factors for individual portfolios. Alpha Streams 1.0 only supported one alpha per live server, but there should be thousands or millions of these factors, each much smaller and focused on a specific idea. Ideally, we should support running hundreds of these factors from a single live-host server.

What does this mean for current investors?

- Alpha renewals have been disabled, and we will work with existing longer-term licensing clients to find a solution for their alphas or refund the license.

- Stop any active live trading servers as they will automatically stop in the next few days. Ensure you tidy up any remaining holdings.

- Investors passionate about their current alpha reach out to support@quantconnect.com and we'll assist to arrange a lifetime license to the alpha if the developer is open to it.

What does this mean for authors/engineers?

We're incredibly grateful for those who've worked with QC to make Alpha Streams so far. We hope the reasoning for why we're doing this shines through and you agree it is the best for the investors long term. It will take some time but please bear with us while we refactor the platform.

- All existing license obligations are “relinquished”; we'll contact you if an investor would like a lifetime license.

- We'll work to pay out all existing wallet balances for alpha licenses.

- Alpha live hosts will be stopped in the next week.

Why not just run 1.0 and 2.0 in parallel?

We see some of these issues as too fundamental to keep the system public. In the interest of wanting the best for the investors using QC, keeping their faith in the long-term, and focusing our efforts, we elected for a full stop. The ultimate result of the overfitting is generally poor performance out-of-sample which makes it hard for us to promote in good conscience.

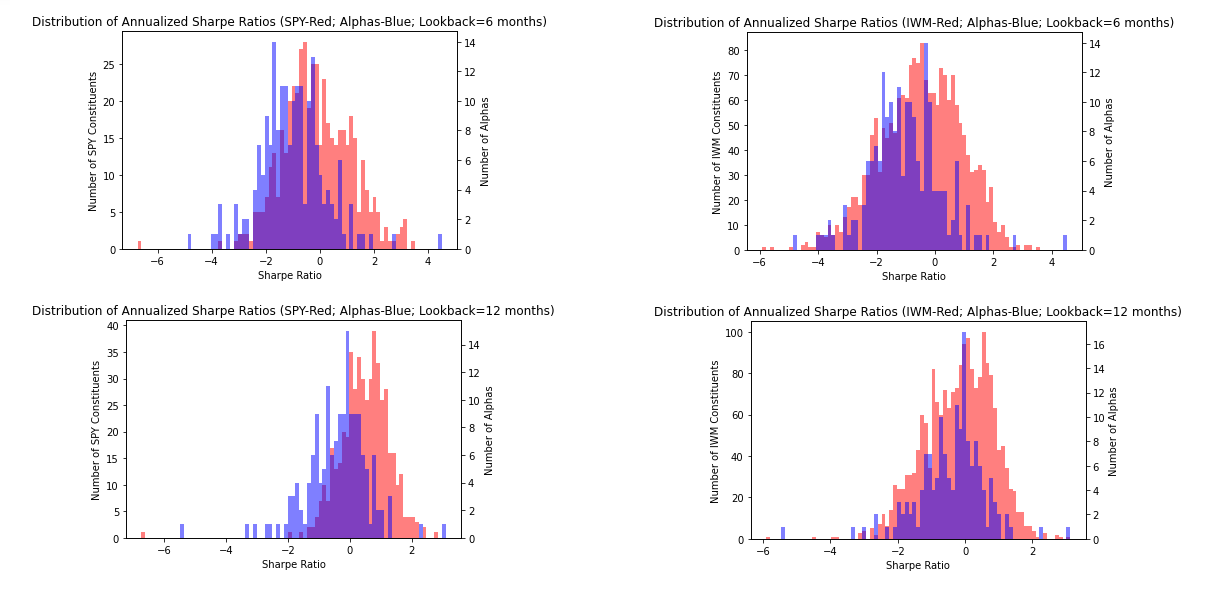

Negative Skew of Alpha Sharpe Ratios vs S&P500 or Russel Constituents

Negative Skew of Alpha Sharpe Ratios vs S&P500 or Russel Constituents (6mo)

To measure the performance we compared distributions of the Alphas Sharpe Ratio with S&P500 and Russel constituents. As seen above, there was a population shift negative(blue=alphas) which made constructing a portfolio of alphas difficult. We researched taking a “needle in a haystack” approach and only selecting the top 5% of the Alpha Market but after eliminating illiquid alphas, and a few crypto outliers, the remaining alphas underperformed the S&P500. We also explored taking uncorrelated alphas and adding them to a broad market portfolio to complement performance but they were not additive.

I know it is tough news for many who've invested months in designing and submitting Alphas. It will take some time but we will carry those skills over into the new Alpha 2.0 platform. The new version will adapt lessons from the industry's titans such as Rentech who've used this style of investing successfully for 30 years. We will be the first to bring this to the wider investor market with the help of an awesome community to create the millions of factors needed. This technology could be used for QC Alpha Streams or independent quant firms building on QC infrastructure. Feel free to ask any questions here and we'll do our best to answer them,

Best,

Jared

AK M

Yeah tough decision, but makes sense given the data.

Can you pin this? Right now I don't think this thread has a lot of visibility.

Does this change have an impact on how the Alpha Framework development will work? Are we still able to select assets if we want, not for alpha streams but for our own live trading? How would alphas that require a fixed set of symbols work (ETF baskets, pairs) if symbols are anonymized?

Jared Broad

There would be no changes to the core QC infrastructure such as live trading, this is purely Alpha Streams. The Algorithm Framework will still operate as is, and I think the new 2.0 would use the Alpha Models as a way to submit factors. This way people could design and use factors for themselves, or submit them to the community pool of factors without needing code changes.

Alpha requiring baskets are probably fine as long as the smallest basket is say the S&P500, but ideally, I think the Alphas would aim to generate signals for all assets when appropriate.

The material on this website is provided for informational purposes only and does not constitute an offer to sell, a solicitation to buy, or a recommendation or endorsement for any security or strategy, nor does it constitute an offer to provide investment advisory services by QuantConnect. In addition, the material offers no opinion with respect to the suitability of any security or specific investment. QuantConnect makes no guarantees as to the accuracy or completeness of the views expressed in the website. The views are subject to change, and may have become unreliable for various reasons, including changes in market conditions or economic circumstances. All investments involve risk, including loss of principal. You should consult with an investment professional before making any investment decisions.

Ross Wendt

This looks like the right move given the performance of current Alpha. I support it, though it does suck as someone new to the platform and pushing over the past month to try to get their first Alpha approved.

I am looking forward to Alpha Streams 2.0 and I hope it will generate a lot more usable Alpha. That will expand QuantConnect in the right direction for everyone!

Rémy Heinis

Good move, that is needed.

Do you have a time line of when this version 2 would be available?

Malcolm Me

Looks good!

ATK23

Hi Jared - I support this decision! Painful, but the right thing to do and I commend you guys for it. Do you have an estimated timeline for for launch of v2? In the interim, do you intend to reduce the monthly pricing given its not possible to license alpha's?

Cole S

100% support this decision, it's needed. My current work revolves around this same concept of having numerous Alpha/Factors working together.

Jared Broad

It'll require some research so we're estimating at least 6 months which would put us into September-October. We disabled the sales of Alpha Streams entirely in the meantime.

The material on this website is provided for informational purposes only and does not constitute an offer to sell, a solicitation to buy, or a recommendation or endorsement for any security or strategy, nor does it constitute an offer to provide investment advisory services by QuantConnect. In addition, the material offers no opinion with respect to the suitability of any security or specific investment. QuantConnect makes no guarantees as to the accuracy or completeness of the views expressed in the website. The views are subject to change, and may have become unreliable for various reasons, including changes in market conditions or economic circumstances. All investments involve risk, including loss of principal. You should consult with an investment professional before making any investment decisions.

Ashraf Said

pls , pls read the book “ Safe Havens , Investing for financial storms ” as it may provide you -as it did with me- with very useful and practical insights , so that Alpha 2. 0 can serve as a relatively secure safe harbor and not just haven and best of luck going forward

GEightyFour

I really appreciate that your team is working on improving the Alpha Universes but is there any work on adding Fundamental History for the backtesting/live framework? I see a world of potential Alpha that's missing out by not having that feature.

Jared Broad

Hi GEightyFour – we are shipping a big update to WarmUp that allows it to use universes. This would be a step in the right direction for fundamental history. We don't quite have a “history request” for fundamentals but this can be added to the todo list :)

The material on this website is provided for informational purposes only and does not constitute an offer to sell, a solicitation to buy, or a recommendation or endorsement for any security or strategy, nor does it constitute an offer to provide investment advisory services by QuantConnect. In addition, the material offers no opinion with respect to the suitability of any security or specific investment. QuantConnect makes no guarantees as to the accuracy or completeness of the views expressed in the website. The views are subject to change, and may have become unreliable for various reasons, including changes in market conditions or economic circumstances. All investments involve risk, including loss of principal. You should consult with an investment professional before making any investment decisions.

Ashraf Said

HI everyone , HI Jared

am looking keenly in to the following improvements if possible within your update review , as these in my modest view have an effect in terms of productivity of building new alpha streams

1- access to more markets with different asset classes and geographies with relatively stable backing of fiat currencies

2- possibility of adding an indicator of the shorting cost per day (in dollars or percents) of each shortable instrument within the universe available on QC platform

3- adding a battery of automatic statistical verification tools to verify if trading / or an investment idea can produce statistically significant stream of returns relative to and better than a certain benchmark

4- adding funds flow data with at least daily update if possible ( basically for ETFs ) , basically as a conditioner for regimes hence as a risk management tool

wishing the best going forward with your efforts in letting that happen

Anshul Vishwakarma

Hi Jared - has there been any updates to the release date of Alpha Streams 2.0? Thanks

Jared Broad

Hi Anshul - we're launching a fundraising campaign shortly. Once its complete we'll have a better picture of the timeline for V2. With an unlimited budget, it would be about 6 months of work if we started today. Alpha Streams is a stretch project for QuantConnect, so we will need success in fundraising to give us the buffer.

The material on this website is provided for informational purposes only and does not constitute an offer to sell, a solicitation to buy, or a recommendation or endorsement for any security or strategy, nor does it constitute an offer to provide investment advisory services by QuantConnect. In addition, the material offers no opinion with respect to the suitability of any security or specific investment. QuantConnect makes no guarantees as to the accuracy or completeness of the views expressed in the website. The views are subject to change, and may have become unreliable for various reasons, including changes in market conditions or economic circumstances. All investments involve risk, including loss of principal. You should consult with an investment professional before making any investment decisions.

Spencer Wasden

It would be nice on these pages if there was some kind of status, plan, hope….something…for v2 and possibly a link to this community page. I've been away for a while so I didn't realize all of this until I dug a bit.

https://www.quantconnect.com/alphastreams

https://www.quantconnect.com/market/

Jared Broad

Thanks for letting us know about those pages Spencer - we'll redirect those landing pages to this forum.

Regarding timeline and plan, it's a more speculative project, so a lot depends on the progress of our fundraise. If we can secure the funding it provides bandwidth for projects like Alpha Streams.

The material on this website is provided for informational purposes only and does not constitute an offer to sell, a solicitation to buy, or a recommendation or endorsement for any security or strategy, nor does it constitute an offer to provide investment advisory services by QuantConnect. In addition, the material offers no opinion with respect to the suitability of any security or specific investment. QuantConnect makes no guarantees as to the accuracy or completeness of the views expressed in the website. The views are subject to change, and may have become unreliable for various reasons, including changes in market conditions or economic circumstances. All investments involve risk, including loss of principal. You should consult with an investment professional before making any investment decisions.

Andres Arizpe

Hi Jared,

Very interested in the Alpha Streams market and have not seen any updates in 10 months.

Could you please provide one?

Thanks,

AA

Vadim Demesy

Hi,

I would like to do the backtest of some futures. I found there are many missing data on “CC (Cocoa (NYCSCE) Futures)”, “DX (US Dollar Index (Futures))”.

Is it normal? Or I need to pay for the data?

Maryam

Hi, I am new to this community. I just want to know if Alpha Stream is still alive or it is pulled.

Christian Krogh

Any news on the Alpha Streams 2.0 do you have a ETA on relaunching the program ?

Jared Broad

The material on this website is provided for informational purposes only and does not constitute an offer to sell, a solicitation to buy, or a recommendation or endorsement for any security or strategy, nor does it constitute an offer to provide investment advisory services by QuantConnect. In addition, the material offers no opinion with respect to the suitability of any security or specific investment. QuantConnect makes no guarantees as to the accuracy or completeness of the views expressed in the website. The views are subject to change, and may have become unreliable for various reasons, including changes in market conditions or economic circumstances. All investments involve risk, including loss of principal. You should consult with an investment professional before making any investment decisions.

To unlock posting to the community forums please complete at least 30% of Boot Camp.

You can continue your Boot Camp training progress from the terminal. We hope to see you in the community soon!