Applying Research

Mean Reversion

Create Hypothesis

Imagine that we've developed the following hypothesis: stocks that are below 1 standard deviation of their 30-day-mean are due to revert and increase in value, statistically around 85% chance if we assume the return series is stationary and the price series is a Random Process. We've developed the following code in research to pick out such stocks from a preselected basket of stocks.

Import Libraries

Load the required assembly files and data types.

We'll need to import libraries to help with data processing. Import numpy and scipy libraries by the following:

// Load the required assembly files and data types in a separate cell. #load "../Initialize.csx"

// Load the necessary assembly files. #load "../QuantConnect.csx"

using QuantConnect; using QuantConnect.Data; using QuantConnect.Data.Market; using QuantConnect.Algorithm; using QuantConnect.Research; using System; using MathNet.Numerics.Distributions;

import numpy as np from scipy.stats import norm, zscore

Get Historical Data

To begin, we retrieve historical data for researching.

- Instantiate a

QuantBook. - Select the desired tickers for research.

- Call the

AddEquityadd_equitymethod with the tickers, and their corresponding resolution. - Call the

Historyhistorymethod withqb.Securities.Keysqb.securities.keysfor all tickers, time argument(s), and resolution to request historical data for the symbol.

var qb = new QuantBook();

qb = QuantBook()

var assets = new List<string>() {"SHY", "TLT", "SHV", "TLH", "EDV", "BIL",

"SPTL", "TBT", "TMF", "TMV", "TBF", "VGSH", "VGIT",

"VGLT", "SCHO", "SCHR", "SPTS", "GOVT"}; assets = ["SHY", "TLT", "SHV", "TLH", "EDV", "BIL",

"SPTL", "TBT", "TMF", "TMV", "TBF", "VGSH", "VGIT",

"VGLT", "SCHO", "SCHR", "SPTS", "GOVT"]

foreach(var ticker in assets){

qb.AddEquity(ticker, Resolution.Minute);

} for i in range(len(assets)):

qb.add_equity(assets[i],Resolution.MINUTE)

If you do not pass a resolution argument, Resolution.MinuteResolution.MINUTE is used by default.

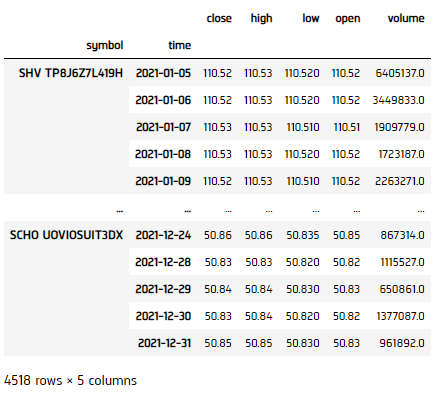

var history = qb.History(qb.Securities.Keys, new DateTime(2021, 1, 1), new DateTime(2021, 12, 31), Resolution.Daily);

history = qb.history(qb.securities.keys(), datetime(2021, 1, 1), datetime(2021, 12, 31), Resolution.DAILY)

Prepare Data

We'll have to process our data to get an extent of the signal on how much the stock is deviated from its norm for each ticker.

- Extract close prices for each

SymbolfromSlicedata. - Select the close column and then call the

unstackmethod. - Get the 30-day rolling mean, standard deviation series, z-score and filtration for each

Symbol. - Calculate the truth value of the most recent price being less than 1 standard deviation away from the mean price.

- Calculate the expected return and its probability, then calculate the weight.

- Get the z-score for the True values, then compute the expected return and probability (used for Insight magnitude and confidence).

- Convert the weights into 2-d array.

- Call

fillnato fill NaNs with 0. - Get our trading weight, we'd take a long only portfolio and normalized to total weight = 1.

var closes = new Dictionary<Symbol, List<Decimal>>();

foreach(var slice in history){

foreach(var symbol in slice.Keys){

if(!closes.ContainsKey(symbol)){

closes.Add(symbol, new List<Decimal>());

}

closes[symbol].Add(slice.Bars[symbol].Close);

}

} df = history['close'].unstack(level=0)

var rollingMean = new Dictionary<Symbol, List<double>>();

var rollingStd = new Dictionary<Symbol, List<double>>();

var filter = new Dictionary<Symbol, List<bool>>();

var zScore = new Dictionary<Symbol, List<double>>();

foreach(var kvp in closes)

{

var symbol = kvp.Key;

if(!rollingMean.ContainsKey(symbol)){

rollingMean.Add(symbol, new List<double>());

rollingStd.Add(symbol, new List<double>());

zScore.Add(symbol, new List<double>());

filter.Add(symbol, new List<bool>());

}

for (int i=30; i < closes.Values.ElementAt(0).Count; i++)

{

var slice = kvp.Value.Skip(i).Take(30);

rollingMean[symbol].Add(decimal.ToDouble(slice.Average()));

rollingStd[symbol].Add(Math.Sqrt(slice.Average(v => Math.Pow(decimal.ToDouble(v-slice.Average()), 2))));

zScore[symbol].Add((decimal.ToDouble(closes[symbol][i]) - rollingMean[symbol].Last()) / rollingStd[symbol].Last());

filter[symbol].Add(zScore[symbol].Last() < -1);

}

} classifier = df.le(df.rolling(30).mean() - df.rolling(30).std())

var magnitude = new Dictionary<Symbol, List<double>>();

var confidence = new Dictionary<Symbol, List<double>>();

var weights = new Dictionary<Symbol, List<double>>();

foreach(var kvp in rollingMean)

{

var symbol = kvp.Key;

if(!magnitude.ContainsKey(symbol)){

magnitude.Add(symbol, new List<double>());

confidence.Add(symbol, new List<double>());

weights.Add(symbol, new List<double>());

}

for (int i=1; i < rollingMean.Values.ElementAt(0).Count; i++)

{

magnitude[symbol].Add(-zScore[symbol][i] * rollingStd[symbol][i] / decimal.ToDouble(closes[symbol][i-1]));

confidence[symbol].Add(Normal.CDF(0, 1, -zScore[symbol][i]));

// Filter if trade or not

var trade = filter[symbol][i] ? 1d : 0d;

weights[symbol].Add(trade * Math.Max(confidence[symbol].Last() - 1 / (magnitude[symbol].Last() + 1), 0));

}

} z_score = df.apply(zscore)[classifier] magnitude = -z_score * df.rolling(30).std() / df.shift(1) confidence = (-z_score).apply(norm.cdf)

double[,] weight = new double[weights.Values.ElementAt(0).Count, weights.Count];

int j = 0;

foreach(var symbol in weights.Keys){

for(int i=0; i < weights[symbol].Count; i++){

weight[i, j] = weights[symbol][i];

}

j++;

} magnitude.fillna(0, inplace=True) confidence.fillna(0, inplace=True)

public double[,] Normalize(double[,] array)

{

for(int i=0; i < array.GetLength(0); i++)

{

var sum = 0.0;

for (int j=0; j < array.GetLength(1); j++)

{

sum += array[i, j];

}

if (sum == 0.0) continue;

for (int j=0; j < array.GetLength(1); j++)

{

array[i, j] = array[i, j] / sum;

}

}

return array;

}

weight = Normalize(weight); weight = confidence - 1 / (magnitude + 1)

weight = weight[weight > 0].fillna(0)

sum_ = np.sum(weight, axis=1)

for i in range(weight.shape[0]):

if sum_[i] > 0:

weight.iloc[i] = weight.iloc[i] / sum_[i]

else:

weight.iloc[i] = 0

weight = weight.iloc[:-1]

Test Hypothesis

We would test the performance of this strategy. To do so, we would make use of the calculated weight for portfolio optimization.

- Convert close price to 2-d array.

- Get the total daily return series.

- Call

cumprodto get the cumulative return. - Set index for visualization.

- Display the result.

double[,] close = new double[closes.Values.ElementAt(0).Count, closes.Count];

int j = 0;

foreach(var symbol in closes.Keys){

for(int i=0; i < closes[symbol].Count; i++){

close[i, j] = decimal.ToDouble(closes[symbol][i]);

}

j++;

}

var totalValue = new List<double>{1.0};

var dailySum = 0.0;

for(int i=0; i < weight.GetLength(0) - 1; i++)

{

totalValue.Add(totalValue.Last() * (1 + dailySum));

dailySum = 0.0;

for (int j=0; j < weight.GetLength(1); j++)

{

if (close[i, j] != 0 && double.IsFinite(close[i+1, j]) && double.IsFinite(close[i, j]) && double.IsFinite(weight[i, j]))

{

dailySum += weight[i, j] * (close[i+1, j] - close[i, j]) / close[i, j];

}

}

} ret = pd.Series(index=range(df.shape[0] - 1))

for i in range(df.shape[0] - 1):

ret[i] = weight.iloc[i] @ df.pct_change().iloc[i + 1].T

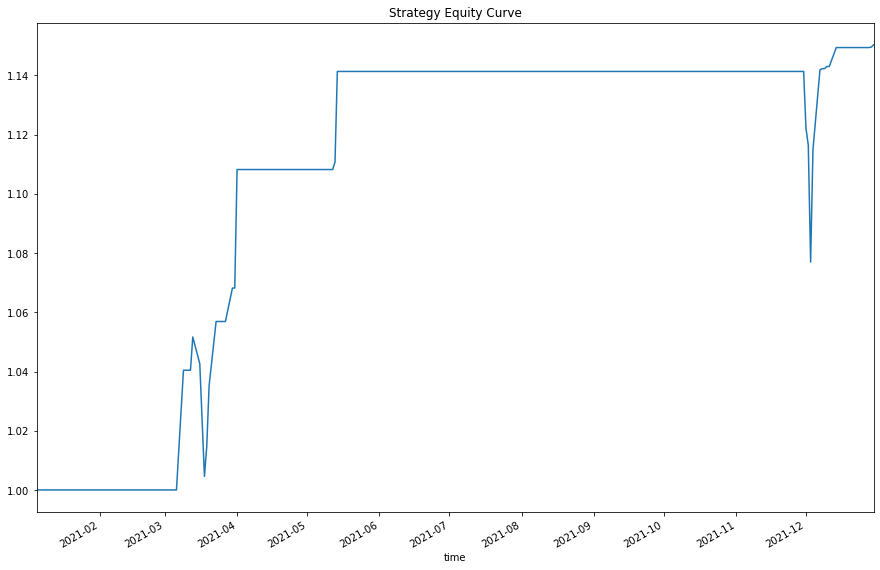

total_ret = (ret + 1).cumprod()

total_ret.index = weight.index

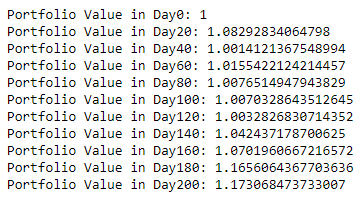

for(int i=0; i < totalValue.Count; i=i+5)

{

Console.WriteLine("Portfolio Value in Day{0}: {1}", i, totalValue[i]);

} total_ret.plot(title='Strategy Equity Curve', figsize=(15, 10)) plt.show()

Set Up Algorithm

Once we are confident in our hypothesis, we can export this code into backtesting. One way to accomodate this model into research is to create a scheduled event which uses our model to pick stocks and goes long.

private List<string> _asset = new List<string>{"SHY", "TLT", "IEI", "SHV", "TLH", "EDV", "BIL",

"SPTL", "TBT", "TMF", "TMV", "TBF", "VGSH", "VGIT",

"VGLT", "SCHO", "SCHR", "SPTS", "GOVT"};

public override void Initialize()

{

// 1. Required: Five years of backtest history

SetStartDate(2014, 1, 1);

// 2. Required: Alpha Streams Models:

SetBrokerageModel(BrokerageName.AlphaStreams);

// 3. Required: Significant AUM Capacity

SetCash(1000000);

// 4. Required: Benchmark to SPY

SetBenchmark("SPY");

SetPortfolioConstruction(new InsightWeightingPortfolioConstructionModel());

SetExecution(new ImmediateExecutionModel());

// Add Equity ------------------------------------------------

foreach(var ticker in _asset)

{

AddEquity(ticker, Resolution.Minute);

}

// Set Scheduled Event Method For Our Model

Schedule.On(DateRules.EveryDay(),

TimeRules.BeforeMarketClose("SHY", 5),

EveryDayBeforeMarketClose);

} def initialize(self) -> None:

#1. Required: Five years of backtest history

self.set_start_date(2014, 1, 1)

#2. Required: Alpha Streams Models:

self.set_brokerage_model(BrokerageName.ALPHA_STREAMS)

#3. Required: Significant AUM Capacity

self.set_cash(1000000)

#4. Required: Benchmark to SPY

self.set_benchmark("SPY")

self.set_portfolio_construction(InsightWeightingPortfolioConstructionModel())

self.set_execution(ImmediateExecutionModel())

self.assets = ["SHY", "TLT", "IEI", "SHV", "TLH", "EDV", "BIL",

"SPTL", "TBT", "TMF", "TMV", "TBF", "VGSH", "VGIT",

"VGLT", "SCHO", "SCHR", "SPTS", "GOVT"]

# Add Equity ------------------------------------------------

for i in range(len(self.assets)):

self.add_equity(self.assets[i], Resolution.MINUTE)

# Set Scheduled Event Method For Our Model

self.schedule.on(self.date_rules.every_day(), self.time_rules.before_market_close("SHY", 5), self.every_day_before_market_close)

Now we export our model into the scheduled event method. We will remove qb and replace methods with their QCAlgorithm counterparts as needed. In this example, this is not an issue because all the methods we used in research also exist in QCAlgorithm.

Now we export our model into the scheduled event method. We will switch qb with self and replace methods with their QCAlgorithm counterparts as needed. In this example, this is not an issue because all the methods we used in research also exist in QCAlgorithm.

private void EveryDayBeforeMarketClose()

{

// Fetch history on our universe

var history = History(Securities.Keys, 30, Resolution.Daily);

if (history.Count() < 0) return;

// Extract close prices for each Symbol from Slice data

var closes = new Dictionary<Symbol, List<Decimal>>();

foreach(var slice in history){

foreach(var symbol in slice.Keys){

if(!closes.ContainsKey(symbol)){

closes.Add(symbol, new List<Decimal>());

}

closes[symbol].Add(slice.Bars[symbol].Close);

}

}

// Get the 30-day rolling mean, standard deviation series, z-score and filtration for each Symbol

var rollingMean = new Dictionary<string, double>();

var rollingStd = new Dictionary<string, double>();

var filter = new Dictionary<string, bool>();

var zScore = new Dictionary<string, double>();

foreach(var kvp in closes)

{

var symbol = kvp.Key;

if(!rollingMean.ContainsKey(symbol)){

rollingMean.Add(symbol, decimal.ToDouble(kvp.Value.Average()));

rollingStd.Add(symbol, Math.Sqrt(kvp.Value.Average(v => Math.Pow(decimal.ToDouble(v-kvp.Value.Average()), 2))));

zScore.Add(symbol, (decimal.ToDouble(kvp.Value.Last()) - rollingMean[symbol]) / rollingStd[symbol]);

filter.Add(symbol, zScore[symbol] < -1);

}

}

// Calculate the expected return and its probability, then calculate the weight

var magnitude = new Dictionary<Symbol, double>();

var confidence = new Dictionary<Symbol, double>();

var weights = new Dictionary<Symbol, double>();

foreach(var kvp in rollingMean)

{

var symbol = kvp.Key;

if(!magnitude.ContainsKey(symbol)){

magnitude.Add(symbol, -zScore[symbol] * rollingStd[symbol] / decimal.ToDouble(closes[symbol].Last()));

confidence.Add(symbol, Normal.CDF(0, 1, -zScore[symbol]));

// Filter if trade or not

var trade = filter[symbol] ? 1d : 0d;

weights.Add(symbol, trade * Math.Max(confidence[symbol] - 1 / (magnitude[symbol] + 1), 0));

}

}

// Normalize the weights, then emit insights

var sum = weights.Sum(x => x.Value);

if (sum == 0) return;

foreach(var kvp in weights)

{

var symbol = kvp.Key;

weights[symbol] = kvp.Value / sum;

var insight = new Insight(symbol, TimeSpan.FromDays(1), InsightType.Price, InsightDirection.Up, magnitude[symbol], confidence[symbol], null, weights[symbol]);

EmitInsights(insight);

}

} def every_day_before_market_close(self) -> None:

qb = self

# Fetch history on our universe

df = qb.history(list(qb.securities.keys()), 30, Resolution.DAILY)

if df.empty: return

# Make all of them into a single time index.

df = df.close.unstack(level=0)

# Calculate the truth value of the most recent price being less than 1 std away from the mean

classifier = df.le(df.mean().subtract(df.std())).iloc[-1]

if not classifier.any(): return

# Get the z-score for the True values, then compute the expected return and probability

z_score = df.apply(zscore)[[classifier.index[i] for i in range(classifier.size) if classifier.iloc[i]]]

magnitude = -z_score * df.std() / df

confidence = (-z_score).apply(norm.cdf)

# Get the latest values

magnitude = magnitude.iloc[-1].fillna(0)

confidence = confidence.iloc[-1].fillna(0)

# Get the weights, then zip together to iterate over later

weight = confidence - 1 / (magnitude + 1)

weight = weight[weight > 0].fillna(0)

sum_ = np.sum(weight)

if sum_ > 0:

weight = (weight) / sum_

selected = zip(weight.index, magnitude, confidence, weight)

else:

return

# ==============================

insights = []

for symbol, magnitude, confidence, weight in selected:

insights.append( Insight.price(symbol, timedelta(days=1), InsightDirection.UP, magnitude, confidence, None, weight) )

self.emit_insights(insights)

Examples

The below code snippets concludes the above jupyter research notebook content.

// Load the required assembly files and data types. #load "../Initialize.csx"

// Load the necessary assembly files. #load "../QuantConnect.csx"

using QuantConnect;

using QuantConnect.Data;

using QuantConnect.Data.Market;

using QuantConnect.Algorithm;

using QuantConnect.Research;

using System;

using MathNet.Numerics.Distributions;

// Instantiate a QuantBook

var qb = new QuantBook();

// Select the desired tickers for research.

var assets = new List<string>() {"SHY", "TLT", "SHV", "TLH", "EDV", "BIL",

"SPTL", "TBT", "TMF", "TMV", "TBF", "VGSH", "VGIT",

"VGLT", "SCHO", "SCHR", "SPTS", "GOVT"};

// Call the AddEquity method with the tickers, and their corresponding resolution.

foreach(var ticker in assets){

qb.AddEquity(ticker, Resolution.Minute);

}

// Call the History method with qb.Securities.Keys for all tickers, time argument(s), and resolution to request historical data for the symbol.

var history = qb.History(qb.Securities.Keys, new DateTime(2020, 1, 1), new DateTime(2022, 1, 1), Resolution.Daily);

// Extract close prices for each Symbol from Slice data

var closes = new Dictionary<Symbol, List<Decimal>>();

foreach(var slice in history){

foreach(var symbol in slice.Keys){

if(!closes.ContainsKey(symbol)){

closes.Add(symbol, new List<Decimal>());

}

closes[symbol].Add(slice.Bars[symbol].Close);

}

}

// Get the 30-day rolling mean, standard deviation series, z-score and filtration for each Symbol

var rollingMean = new Dictionary<Symbol, List<double>>();

var rollingStd = new Dictionary<Symbol, List<double>>();

var filter = new Dictionary<Symbol, List<bool>>();

var zScore = new Dictionary<Symbol, List<double>>();

foreach(var kvp in closes)

{

var symbol = kvp.Key;

if(!rollingMean.ContainsKey(symbol)){

rollingMean.Add(symbol, new List<double>());

rollingStd.Add(symbol, new List<double>());

zScore.Add(symbol, new List<double>());

filter.Add(symbol, new List<bool>());

}

for (int i=30; i < closes.Values.ElementAt(0).Count; i++)

{

var slice = kvp.Value.Skip(i).Take(30);

rollingMean[symbol].Add(decimal.ToDouble(slice.Average()));

rollingStd[symbol].Add(Math.Sqrt(slice.Average(v => Math.Pow(decimal.ToDouble(v-slice.Average()), 2))));

zScore[symbol].Add((decimal.ToDouble(closes[symbol][i]) - rollingMean[symbol].Last()) / rollingStd[symbol].Last());

filter[symbol].Add(zScore[symbol].Last() < -1);

}

}

// Calculate the expected return and its probability, then calculate the weight

var magnitude = new Dictionary<Symbol, List<double>>();

var confidence = new Dictionary<Symbol, List<double>>();

var weights = new Dictionary<Symbol, List<double>>();

foreach(var kvp in rollingMean)

{

var symbol = kvp.Key;

if(!magnitude.ContainsKey(symbol)){

magnitude.Add(symbol, new List<double>());

confidence.Add(symbol, new List<double>());

weights.Add(symbol, new List<double>());

}

for (int i=1; i < rollingMean.Values.ElementAt(0).Count; i++)

{

magnitude[symbol].Add(-zScore[symbol][i] * rollingStd[symbol][i] / decimal.ToDouble(closes[symbol][i]));

confidence[symbol].Add(Normal.CDF(0, 1, -zScore[symbol][i]));

//Filter if trade or not

var trade = filter[symbol][i] ? 1d : 0d;

weights[symbol].Add(trade * Math.Max(confidence[symbol].Last() - 1 / (magnitude[symbol].Last() + 1), 0));

}

}

// Convert the weights into 2-d array

double[,] weight = new double[weights.Values.ElementAt(0).Count, weights.Count];

int j = 0;

foreach(var symbol in weights.Keys){

for(int i=0; i < weights[symbol].Count; i++){

weight[i, j] = weights[symbol][i];

}

j++;

}

// Normalize the weights

public double[,] Normalize(double[,] array)

{

for(int i=0; i < array.GetLength(0); i++)

{

var sum = 0.0;

for (int j=0; j < array.GetLength(1); j++)

{

sum += array[i, j];

}

if (sum == 0.0) continue;

for (int j=0; j < array.GetLength(1); j++)

{

array[i, j] = array[i, j] / sum;

}

}

return array;

}

weight = Normalize(weight);

// Convert close price to 2-d array

double[,] close = new double[closes.Values.ElementAt(0).Count, closes.Count];

int j = 0;

foreach(var symbol in closes.Keys){

for(int i=0; i < closes[symbol].Count; i++){

close[i, j] = decimal.ToDouble(closes[symbol][i]);

}

j++;

}

// Get daily total forward return series

var totalValue = new List<double>{1.0};

var dailySum = 0.0;

for(int i=0; i < weight.GetLength(0) - 1; i++)

{

totalValue.Add(totalValue.Last() * (1 + dailySum));

dailySum = 0.0;

for (int j=0; j < weight.GetLength(1); j++)

{

if (close[i, j] != 0 && double.IsFinite(close[i+1, j]) && double.IsFinite(close[i, j]) && double.IsFinite(weight[i, j]))

{

dailySum += weight[i, j] * (close[i+1, j] - close[i, j]) / close[i, j];

}

}

}

// Print the result

for(int i=0; i < totalValue.Count; i=i+20)

{

Console.WriteLine("Portfolio Value in Day{0}: {1}", i, totalValue[i]);

} from scipy.stats import norm, zscore

# Instantiate a QuantBook.

qb = QuantBook()

# Select the desired tickers for research.

symbols = {}

assets = ["SHY", "TLT", "SHV", "TLH", "EDV", "BIL",

"SPTL", "TBT", "TMF", "TMV", "TBF", "VGSH", "VGIT",

"VGLT", "SCHO", "SCHR", "SPTS", "GOVT"]

# Call the AddEquity method with the tickers, and its corresponding resolution. Then store their Symbols. Resolution.Minute is used by default.

for i in range(len(assets)):

symbols[assets[i]] = qb.add_equity(assets[i], Resolution.MINUTE).symbol

# Call the History method with qb.Securities.Keys for all tickers, time argument(s), and resolution to request historical data for the symbol.

history = qb.history(qb.securities.keys(), datetime(2021, 1, 1), datetime(2021, 12, 31), Resolution.DAILY)

# Select the close column and then call the unstack method.

df = history['close'].unstack(level=0)

# Calculate the truth value of the most recent price being less than 1 standard deviation away from the mean price.

classifier = df.le(df.rolling(30).mean() - df.rolling(30).std())

# Get the z-score for the True values, then compute the expected return and probability (used for Insight magnitude and confidence).

z_score = df.apply(zscore)[classifier]

magnitude = -z_score * df.rolling(30).std() / df

confidence = (-z_score).apply(norm.cdf)

# Call fillna to fill NaNs with 0

magnitude.fillna(0, inplace=True)

confidence.fillna(0, inplace=True)

# Get our trading weight, we'd take a long only portfolio and normalized to total weight = 1

weight = confidence - 1 / (magnitude + 1)

weight = weight[weight > 0].fillna(0)

sum_ = np.sum(weight, axis=1)

for i in range(weight.shape[0]):

if sum_[i] > 0:

weight.iloc[i] = weight.iloc[i] / sum_[i]

else:

weight.iloc[i] = 0

weight = weight.iloc[:-1]

# Get the total daily return series

ret = pd.Series(index=range(df.shape[0] - 1))

for i in range(df.shape[0] - 1):

ret[i] = weight.iloc[i] @ df.pct_change().iloc[i + 1].T

# Call cumprod to get the cumulative return

total_ret = (ret + 1).cumprod()

# Set index for visualization

total_ret.index = weight.index

# Plot the result

total_ret.plot(title='Strategy Equity Curve', figsize=(15, 10))

plt.show()

The below code snippets concludes the algorithm set up.

using MathNet.Numerics.Distributions;

public class MeanReversionDemo : QCAlgorithm

{

List<string> _asset = new List<string>{"SHY", "TLT", "IEI", "SHV", "TLH", "EDV", "BIL",

"SPTL", "TBT", "TMF", "TMV", "TBF", "VGSH", "VGIT",

"VGLT", "SCHO", "SCHR", "SPTS", "GOVT"};

public override void Initialize()

{

SetStartDate(2024, 9, 1);

SetEndDate(2024, 12, 31);

SetBrokerageModel(BrokerageName.AlphaStreams);

// Required: Significant AUM Capacity

SetCash(1000000);

// Required: Benchmark to SPY

SetBenchmark("SPY");

SetPortfolioConstruction(new InsightWeightingPortfolioConstructionModel());

SetExecution(new ImmediateExecutionModel());

// Add Equity ------------------------------------------------

foreach(var ticker in _asset)

{

AddEquity(ticker, Resolution.Minute);

}

// Set Scheduled Event Method For Our Model

Schedule.On(DateRules.EveryDay(),

TimeRules.BeforeMarketClose("SHY", 5),

EveryDayBeforeMarketClose);

}

private void EveryDayBeforeMarketClose()

{

// Fetch history on our universe

var history = History(Securities.Keys, 30, Resolution.Daily);

if (history.Count() < 0) return;

// Extract close prices for each Symbol from Slice data

var closes = new Dictionary<Symbol, List<Decimal>>();

foreach(var slice in history){

foreach(var symbol in slice.Keys){

if(!closes.ContainsKey(symbol)){

closes.Add(symbol, new List<Decimal>());

}

closes[symbol].Add(slice.Bars[symbol].Close);

}

}

// Get the 30-day rolling mean, standard deviation series, z-score and filtration for each Symbol

var rollingMean = new Dictionary<string, double>();

var rollingStd = new Dictionary<string, double>();

var filter = new Dictionary<string, bool>();

var zScore = new Dictionary<string, double>();

foreach(var kvp in closes)

{

var symbol = kvp.Key;

if(!rollingMean.ContainsKey(symbol)){

rollingMean.Add(symbol, decimal.ToDouble(kvp.Value.Average()));

rollingStd.Add(symbol, Math.Sqrt(kvp.Value.Average(v => Math.Pow(decimal.ToDouble(v-kvp.Value.Average()), 2))));

zScore.Add(symbol, (decimal.ToDouble(kvp.Value.Last()) - rollingMean[symbol]) / rollingStd[symbol]);

filter.Add(symbol, zScore[symbol] < -1);

}

}

// Calculate the expected return and its probability, then calculate the weight

var magnitude = new Dictionary<Symbol, double>();

var confidence = new Dictionary<Symbol, double>();

var weights = new Dictionary<Symbol, double>();

foreach(var kvp in rollingMean)

{

var symbol = kvp.Key;

if(!magnitude.ContainsKey(symbol)){

magnitude.Add(symbol, -zScore[symbol] * rollingStd[symbol] / decimal.ToDouble(closes[symbol].Last()));

confidence.Add(symbol, Normal.CDF(0, 1, -zScore[symbol]));

// Filter if trade or not

var trade = filter[symbol] ? 1d : 0d;

weights.Add(symbol, trade * Math.Max(confidence[symbol] - 1 / (magnitude[symbol] + 1), 0));

}

}

// Normalize the weights, then emit insights

List<Insight> insights = new List<Insight>{};

var sum = weights.Sum(x => x.Value);

if (sum == 0) return;

foreach(var kvp in weights)

{

var symbol = kvp.Key;

weights[symbol] = kvp.Value / sum / 2d;

var insight = new Insight(symbol, TimeSpan.FromDays(1), InsightType.Price, InsightDirection.Up, magnitude[symbol], confidence[symbol], null, weights[symbol]);

EmitInsights(insight);

}

}

} from scipy.stats import norm, zscore

class MeanReversionDemo(QCAlgorithm):

def initialize(self) -> None:

self.set_start_date(2024, 9, 1)

self.set_end_date(2024, 12, 31)

self.set_brokerage_model(BrokerageName.ALPHA_STREAMS)

# Required: Significant AUM Capacity

self.set_cash(1000000)

# Required: Benchmark to SPY

self.set_benchmark("SPY")

self.set_portfolio_construction(InsightWeightingPortfolioConstructionModel())

self.set_execution(ImmediateExecutionModel())

self.assets = ["SHY", "TLT", "IEI", "SHV", "TLH", "EDV", "BIL",

"SPTL", "TBT", "TMF", "TMV", "TBF", "VGSH", "VGIT",

"VGLT", "SCHO", "SCHR", "SPTS", "GOVT"]

# Add Equity ------------------------------------------------

for i in range(len(self.assets)):

self.add_equity(self.assets[i], Resolution.MINUTE).symbol

# Set Scheduled Event Method For Our Model

self.schedule.on(self.date_rules.every_day(), self.time_rules.before_market_close("SHY", 5), self.every_day_before_market_close)

def every_day_before_market_close(self) -> None:

qb = self

# Fetch history on our universe

df = qb.history(list(qb.securities.keys()), 30, Resolution.DAILY)

if df.empty: return

# Make all of them into a single time index.

df = df.close.unstack(level=0)

# Calculate the truth value of the most recent price being less than 1 std away from the mean

classifier = df.le(df.mean().subtract(df.std())).iloc[-1]

if not classifier.any(): return

# Get the z-score for the True values, then compute the expected return and probability

z_score = df.apply(zscore)[[classifier.index[i] for i in range(classifier.size) if classifier.iloc[i]]]

magnitude = -z_score * df.std() / df

confidence = (-z_score).apply(norm.cdf)

# Get the latest values

magnitude = magnitude.iloc[-1].fillna(0)

confidence = confidence.iloc[-1].fillna(0)

# Get the weights, then zip together to iterate over later

weight = confidence - 1 / (magnitude + 1)

weight = weight[weight > 0].fillna(0)

sum_ = np.sum(weight)

if sum_ > 0:

weight = (weight) / sum_ / 2

selected = zip(weight.index, magnitude, confidence, weight)

else:

return

# ==============================

insights = []

for symbol, magnitude, confidence, weight in selected:

insights.append( Insight.price(symbol, timedelta(days=1), InsightDirection.UP, magnitude, confidence, None, weight) )

self.emit_insights(insights)

You can also see our Videos. You can also get in touch with us via Discord.

Did you find this page helpful?