Popular Libraries

XGBoost

Create Subscriptions

In the Initializeinitialize method, subscribe to some data so you can train the xgboost model and make predictions.

# Add a security and save a reference to its Symbol.

self._symbol = self.add_equity("SPY", Resolution.DAILY).symbol

Build Models

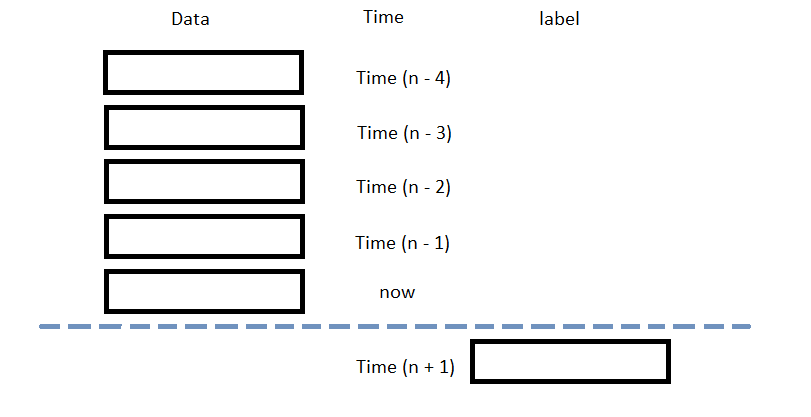

In this example, build a gradient boost tree regression prediction model that uses the following features and labels:

| Data Category | Description |

|---|---|

| Features | The last 5 closing prices |

| Labels | The following day's closing price |

The following image shows the time difference between the features and labels:

Train Models

You can train the model at the beginning of your algorithm and you can periodically re-train it as the algorithm executes.

Warm Up Training Data

You need historical data to initially train the model at the start of your algorithm. To get the initial training data, in the Initializeinitialize method, make a history request.

# Fill a RollingWindow with 2 years of historical closing prices.

training_length = 252*2

self.training_data = RollingWindow(training_length)

history = self.history[TradeBar](self._symbol, training_length, Resolution.DAILY)

for trade_bar in history:

self.training_data.add(trade_bar.close)

Define a Training Method

To train the model, define a method that fits the model with the training data.

# Prepare feature and label data for training by processing the RollingWindow data into a time series.

def get_features_and_labels(self, n_steps=5):

# Create a list of close prices from the rolling window.

close_prices = np.array(list(self.training_data)[::-1])

df = (np.roll(close_prices, -1) - close_prices) * 0.5 + close_prices * 0.5

df = df[:-1]

features = []

labels = []

for i in range(len(df)-n_steps):

features.append(df[i:i+n_steps])

labels.append(df[i+n_steps])

features = np.array(features)

labels = np.array(labels)

# Standardize the features and labels arrays.

features = (features - features.mean()) / features.std()

labels = (labels - labels.mean()) / labels.std()

# Load the NumPy array into a DMatrix object.

d_matrix = xgb.DMatrix(features, label=labels)

return d_matrix

def my_training_method(self):

# Instantiate the DMatrix object with the features and labels array.

d_matrix = self.get_features_and_labels()

# Define the parameters for the XGBoost model.

params = {

'booster': 'gbtree',

'colsample_bynode': 0.8,

'learning_rate': 0.1,

'lambda': 0.1,

'max_depth': 5,

'num_parallel_tree': 100,

'objective': 'reg:squarederror',

'subsample': 0.8,

}

# Create the model and fit it with the training data.

self.model = xgb.train(params, d_matrix, num_boost_round=10)

Set Training Schedule

To train the model at the beginning of your algorithm, in the Initializeinitialize method, call the Traintrain method.

# Train the model initially to provide a baseline for prediction and decision-making. self.train(self.my_training_method)

To periodically re-train the model as your algorithm executes, in the Initializeinitialize method, call the Traintrain method as a Scheduled Event.

# Train the model every Sunday at 8:00 AM. self.train(self.date_rules.every(DayOfWeek.SUNDAY), self.time_rules.at(8, 0), self.my_training_method)

Update Training Data

To update the training data as the algorithm executes, in the OnDataon_data method, add the current TradeBar to the RollingWindow that holds the training data.

# Add the latest price to the training data to ensure the model is trained with the most recent market data.

def on_data(self, slice: Slice) -> None:

if self._symbol in slice.bars:

# Update the training data with new most recent close price.

self.training_data.add(slice.bars[self._symbol].close)

Predict Labels

To predict the labels of new data, in the OnDataon_data method, get the most recent set of features and then call the predict method.

# Get the current feature set and make a prediction. new_d_matrix = self.get_features_and_labels(df) prediction = self.model.predict(new_d_matrix) prediction = prediction.flatten()

You can use the label prediction to place orders.

# Place orders based on the forecasted market direction.

if float(prediction[-1]) > float(prediction[-2]):

self.set_holdings(self._symbol, 1)

else:

self.set_holdings(self._symbol, -1)

Save Models

Follow these steps to save xgboost models into the Object Store:

- Set the key name of the model to be stored in the Object Store.

- Call the

GetFilePathget_file_pathmethod with the key. - Call the

dumpmethod the file path.

# Set the key to store the model in the Object Store so you can use it later.

model_key = f"{self.project_id}/model"

# Get the file path to correctly save and access the model in Object Store. file_name = self.object_store.get_file_path(model_key)

This method returns the file path where the model will be stored.

# Serialize the model and save it to the file. joblib.dump(self.model, file_name)

If you dump the model using the joblib module before you save the model, you don't need to retrain the model.

Upload Models

If you train models locally or in another environment, you can upload the model files to the Object Store so your algorithms can use them. Use the model key that matches the key your algorithm expects when it calls object_store.get_file_path.

Follow one of these approaches to upload your model files:

LEAN CLI

Run the lean cloud object-store set command to upload a local file to the Object Store.

$ lean cloud object-store set <projectId>/model <pathTo>/model

Replace <projectId> with your project Id and <pathTo> with the path to the local model file.

Cloud API

Use the Upload Object Store Files endpoint to upload a model file through the API.

Load Models

You can load and trade with pre-trained xgboost models that saved in Object Store. To load a xgboost model from the Object Store, in the Initializeinitialize method, get the file path to the saved model and then call the load method.

# Load the xgboost model from the Object Store to use its saved state and update it with new data if needed.

def initialize(self) -> None:

model_key = f"{self.project_id}/model"

if self.object_store.contains_key(model_key):

file_name = self.object_store.get_file_path(model_key)

self.model = joblib.load(file_name)

The ContainsKeycontains_key method returns a boolean that represents if the model_key is in the Object Store. If the Object Store does not contain the model_key, save the model using the model_key before you proceed.

Examples

The following examples demonstrate some common practices for using

XGBoost

library.

Example 1: Gradient Boosting Model

The below algorithm makes use of

XGBoost

library to predict the future price movement using the previous 5 OHLCV data. The model is trained using rolling 2-year data. To ensure the model applicable to the current market environment, we recalibrate the model on every Sunday.

import xgboost as xgb

import joblib

class XGBoostExampleAlgorithm(QCAlgorithm):

def initialize(self) -> None:

self.set_start_date(2024, 9, 1)

self.set_end_date(2024, 12, 31)

self.set_cash(100000)

# Request SPY data for model training, prediction and trading.

self._symbol = self.add_equity("SPY", Resolution.DAILY).symbol

# Use the session rolling window to cache 2-year daily data for training.

training_length = 252*2

self.securities[self._symbol].session.size = training_length

self.set_warm_up(training_length, Resolution.DAILY)

# Retrieve already trained model from object store to use immediately.

self._model_key = f"{self.project_id}/xgboost-example-model"

if self.live_mode and self.object_store.contains_key(self._model_key):

file_name = self.object_store.get_file_path(self._model_key)

self.model = joblib.load(file_name)

def on_warmup_finished(self) -> None:

if not hasattr(self, 'model'):

# Train the model to use the prediction right away.

self.train(self.my_training_method)

# Recalibrate the model weekly to ensure its accuracy on the updated domain.

self.train(self.date_rules.every(DayOfWeek.SUNDAY), self.time_rules.at(8,0), self.my_training_method)

def get_features_and_labels(self, n_steps=5) -> None:

# Train and predict the partial-differencing data, which is more stationary while more variance remaining.

close_prices = np.array([x.close for x in self.securities[self._symbol].session][::-1])

df = (np.roll(close_prices, -1) - close_prices) * 0.5 + close_prices * 0.5

df = df[:-1]

# Stack the data for 5-day OHLCV data per each sample to train with.

features = []

labels = []

for i in range(len(df)-n_steps):

features.append(df[i:i+n_steps])

labels.append(df[i+n_steps])

features = np.array(features)

labels = np.array(labels)

features = (features - features.mean()) / features.std()

labels = (labels - labels.mean()) / labels.std()

d_matrix = xgb.DMatrix(features, label=labels)

return d_matrix

def my_training_method(self) -> None:

# Prepare the processed training data.

d_matrix = self.get_features_and_labels()

# Recalibrate the model based on updated data.

params = {

'booster': 'gbtree',

'colsample_bynode': 0.8,

'learning_rate': 0.1,

'lambda': 0.1,

'max_depth': 5,

'num_parallel_tree': 100,

'objective': 'reg:squarederror',

'subsample': 0.8,

}

self.model = xgb.train(params, d_matrix, num_boost_round=2)

def on_data(self, slice: Slice) -> None:

if self.is_warming_up or self._symbol not in slice.bars:

return

# Get prediction by the updated features.

new_d_matrix = self.get_features_and_labels()

prediction = self.model.predict(new_d_matrix)

prediction = prediction.flatten()

# If the predicted direction is going upward, buy SPY.

if float(prediction[-1]) > float(prediction[-2]):

self.set_holdings(self._symbol, 1)

# If the predicted direction is going downward, sell SPY.

else:

self.set_holdings(self._symbol, -1)

def on_end_of_algorithm(self) -> None:

# Store the model to object store to retrieve it in other instances in case the algorithm stops.

if not self.live_mode:

return

file_name = self.object_store.get_file_path(self._model_key)

joblib.dump(self.model, file_name)

self.object_store.save(self._model_key)

You can also see our Videos. You can also get in touch with us via Discord.

Did you find this page helpful?